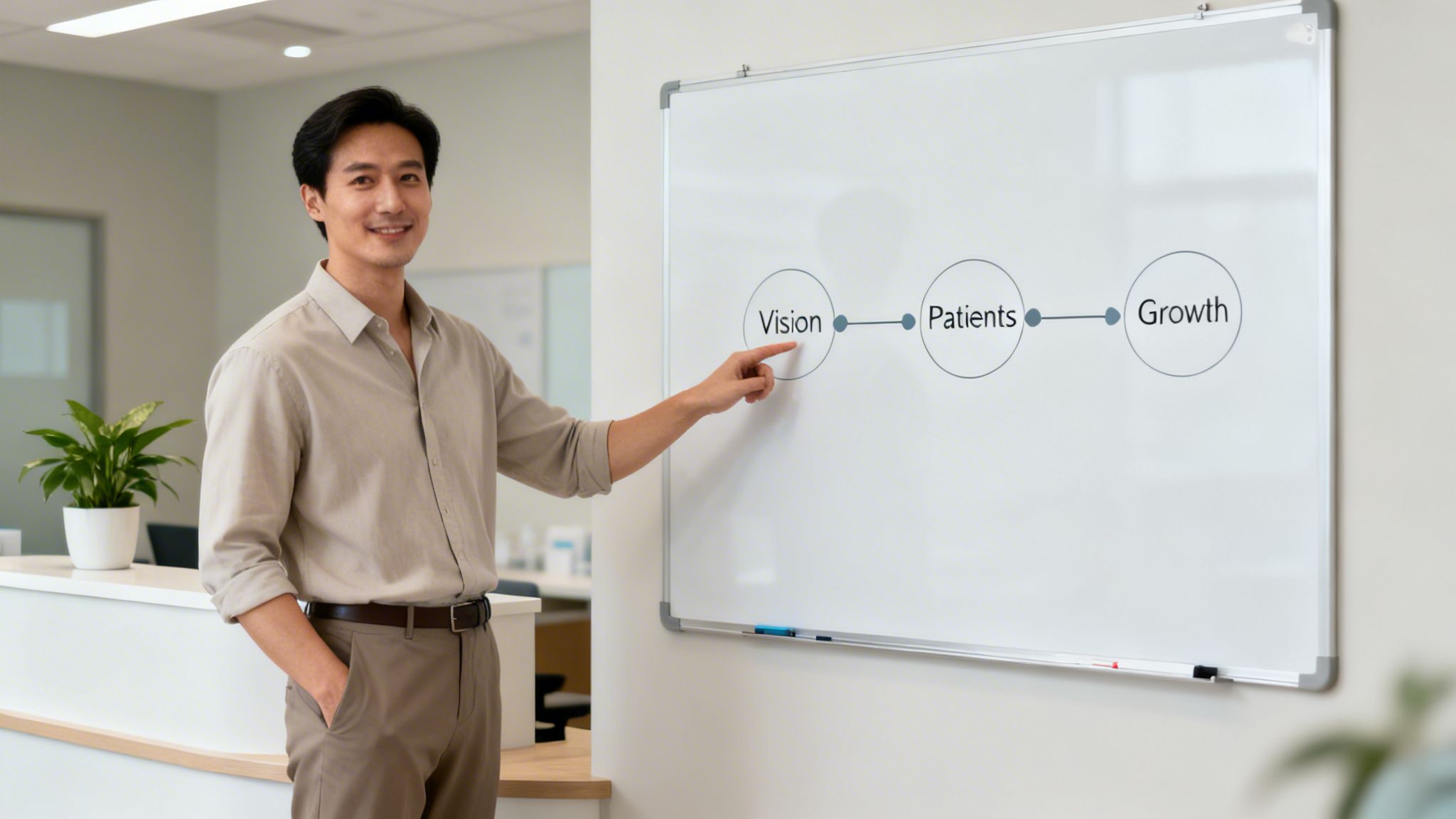

A business plan for your medical practice is so much more than a stuffy document you create just to get a loan. Think of it as your practice's strategic roadmap—the document that defines your vision and guides your clinic toward both profitability and clinical excellence.

It's a living guide that helps you secure funding, yes, but it also attracts top-tier talent and helps you navigate the incredibly competitive healthcare world by forcing you to really analyze your market and plan for smart growth.

Why Your Practice Needs a Dynamic Business Plan

Too many physicians make the mistake of seeing their business plan as a one-and-done task. They write it to satisfy a lender, get the check, and then shove it in a drawer. This is a massive missed opportunity. In today's healthcare market, a well-crafted plan is your most critical management tool. It's the blueprint that transforms your clinical expertise into a sustainable, successful business.

You wouldn't start a complex patient treatment without a detailed plan, right? The exact same logic applies to the health of your business. Your plan provides the clarity and direction needed to ensure every single decision—from who you hire to what technology you invest in—aligns with your long-term goals.

Beyond Securing a Loan

While it's absolutely essential for getting funding, the true value of a business plan for a medical practice goes way beyond the startup phase. It serves several crucial, ongoing strategic purposes:

- Clarifies Your Vision: It forces you to get specific about your mission, define who your ideal patient is, and pinpoint what truly makes your practice different from the one down the street.

- Guides Strategic Decisions: It gives you a framework for evaluating new opportunities, like adding a profitable new service line or expanding to a second location.

- Measures Performance: It sets concrete financial and operational benchmarks. This is how you track progress and spot areas that need a little (or a lot of) improvement before they become big problems.

- Aligns Your Team: A shared vision and clear, written goals ensure your entire staff—from the front desk to your lead practitioners—is pulling in the same direction.

A common pitfall I see is treating the plan as a historical artifact. The most successful practices I've worked with revisit their plans at least annually. They adapt to market shifts, new technologies, and what their patients are asking for. This agility is what separates thriving practices from those that just tread water.

To help you get started, here's a quick-glance summary of the crucial sections your plan needs to effectively communicate your vision to lenders, partners, and your own team.

Essential Components of a Winning Medical Practice Business Plan

| Component | Core Objective | The Critical Question It Answers |

|---|---|---|

| Executive Summary | Provide a compelling, high-level overview of the entire plan. | "Why should I keep reading and invest in this practice?" |

| Market Analysis | Demonstrate deep understanding of the local market, competition, and target patients. | "Is there a real, unmet need for these services in this location?" |

| Services & Pricing | Detail the specific services offered and the pricing strategy behind them. | "What exactly do you sell, and how does it generate revenue?" |

| Operations & Staffing | Outline the day-to-day workflow, key personnel, and organizational structure. | "Who is on the team, and how will the practice actually run?" |

| Compliance Plan | Address all regulatory, licensing, and HIPAA requirements. | "How will you ensure the practice is legal, safe, and compliant?" |

| Financial Projections | Provide detailed startup costs, revenue forecasts, and cash flow analysis. | "Can this practice be profitable, and what are the numbers to prove it?" |

Each of these components tells a critical part of your practice's story, weaving together a narrative that builds confidence and lays the groundwork for success.

The Modern Practice Imperative

For any modern clinic—whether you're a medspa or a highly specialized surgical practice—integrating a smart technology strategy from day one is non-negotiable. Your business plan has to show how you'll use technology to work more efficiently, improve patient care, and keep data secure.

Instead of cobbling together different vendors for your EHR, billing software, and patient communication tools, a forward-thinking plan outlines a unified system. This approach doesn't just make workflows smoother; it cuts down on operational headaches and strengthens your compliance with regulations like HIPAA. It proves to lenders and potential partners that you're building a practice for the future. As your clinic grows, knowing how to manage that expansion becomes absolutely critical, and having the right foundation makes all the difference.

Crafting a Compelling Executive Summary and Mission

Think of your executive summary as the handshake and the entire elevator pitch for your medical practice, all rolled into one. It’s often the only part a busy lender or potential partner will read in full, so it absolutely has to land. This isn't just a dry recap; it's your chance to tell a compelling story about your passion, your market insight, and your financial viability on a single, powerful page.

A huge mistake I see people make is treating this section as an afterthought, something they quickly slap together once the "real" work is done. You have to flip that script. Think of it as the strategic overture that sets the tone for everything that follows. It needs to be clear, confident, and concise, proving you have a firm handle on both the clinical and business sides of your venture.

Defining Your Mission and Vision

Before you even think about writing the summary, you need absolute clarity on your practice’s core purpose. Your mission statement isn’t just some fluffy slogan for your website; it's a declaration of your values and your promise to every patient who walks through your door. It answers the big question: "Why do we exist?"

For instance, a new boutique medspa might build its mission around "empowering individuals through personalized aesthetic treatments that enhance natural beauty and promote self-confidence." That’s a world away from a direct primary care practice whose mission might be to "provide accessible, relationship-based healthcare that prioritizes patient wellness over patient volume."

Your vision statement, on the other hand, is your look into the future. It’s aspirational. It answers, "What do we hope to become?" These two statements are the heart and soul of your executive summary, giving all your financial and operational details a real sense of purpose. Defining this is a crucial step in building your practice's identity, and you can dive deeper into why your practice's branding is so important.

Key Elements to Include

Your executive summary needs to be a highlight reel of the most critical parts of your business plan. It has to flow naturally and tell a complete, albeit brief, story.

- The Problem: What specific gap or unmet need in the market are you here to fill? Be direct.

- The Solution: In a few sentences, describe your practice and the unique services that will solve that problem.

- Target Market: Who is your ideal patient? Define them and explain why they’ll choose you over the competition.

- Financial Highlights: Give them the bottom line. Summarize your startup funding request, your revenue projections for the first year, and when you realistically expect to turn a profit.

The best executive summaries I’ve ever seen strike a perfect balance between passion and pragmatism. They communicate a genuine commitment to patient care while presenting a sober, well-researched financial case. A lender needs to see both the heart and the head behind the business.

A Tale of Two Summaries

Let’s look at two different practices seeking funding to see how this plays out.

A business plan for a medical practice focused on aesthetics could lead with the $16.7 billion Americans spend on cosmetic procedures and point to specific local demand for non-invasive treatments. Its summary would lean into a unique patient experience, advanced technology, and a sharp marketing plan aimed at an affluent demographic.

Now, consider a new functional medicine clinic. Its summary would instead focus on the rising tide of chronic disease and growing patient frustration with the conventional system. It would highlight a membership-based model, highly personalized treatment protocols, and the founder's specialized expertise as key differentiators.

Both summaries work because they connect a clear market need to a specific, believable business model. That’s what makes for a compelling case and gets you the investment you need.

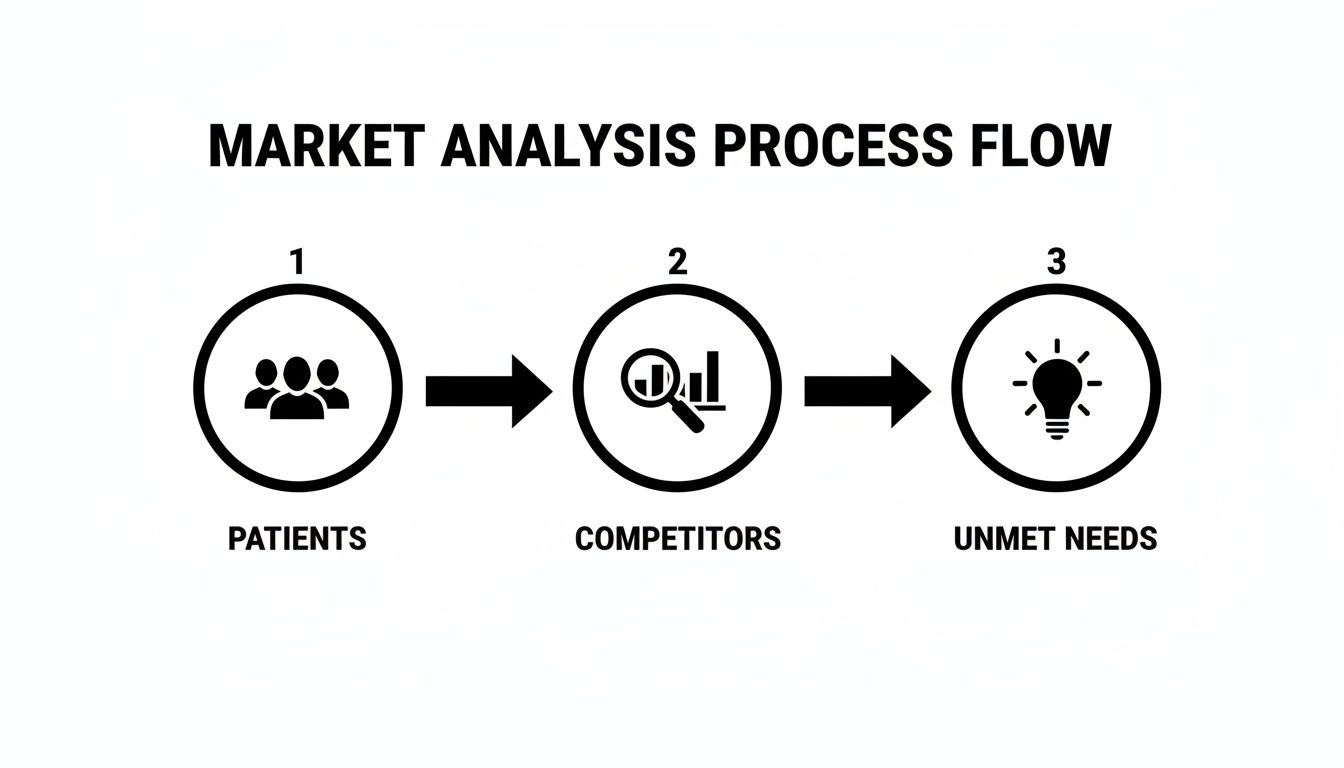

Finding Your Niche: Market Analysis and Competitive Edge

A brilliant idea for a medical practice is just an idea until you can prove it meets a real need in your community. That’s what your market analysis is all about. It’s the hard evidence in your business plan for a medical practice that shows you’ve done your homework and aren’t just guessing. Think of it as moving from a gut feeling to data-driven confidence.

This section proves to lenders and investors that you’re making a calculated move, not a blind bet. It’s where you dig deep into the local healthcare landscape to identify your ideal patients, size up the competition, and find those profitable gaps in care just waiting to be filled.

Who Is Your Ideal Patient?

You can't be everything to everyone. Trying to serve the entire city is a surefire way to spread your resources too thin and make your marketing completely ineffective. The real key is to get incredibly specific about who you want to walk through your doors.

Start building a clear profile of your ideal patient by looking at the details:

- Age and Gender: Are you focused on young families for a pediatric clinic? Or maybe a medspa targeting women aged 30-55?

- Income Level: This is crucial. It directly impacts whether you can focus on cash-based elective procedures or need to navigate a complex web of insurance plans.

- Geographic Location: How far are people willing to drive for your specific services? Define a realistic service area.

- Healthcare Needs: What are the common health issues in your area? Public health data can reveal trends in chronic diseases, wellness interests, or other conditions you can address.

When you have this level of clarity, everything else falls into place. Your service menu, office hours, and marketing messages can all be designed to attract exactly the right people.

Sizing Up the Competition

No practice exists in a bubble. You need an honest, clear-eyed look at the other players in your local market to figure out where you fit in. Your goal is to know who they are, what they do well, and—most importantly—where they’re dropping the ball.

I always tell my clients to create a simple spreadsheet to track this. Start gathering intel on other practices in your chosen service area. Look for:

- Services Offered: Do they offer the same treatments you plan to? Are there any popular services they aren't providing?

- Pricing and Insurance: Find out which insurance plans they accept. If they have cash-pay options, what are their rates?

- Online Presence and Reputation: Dive into their patient reviews on Google, Healthgrades, and Yelp. What do people consistently praise or complain about? This is a goldmine.

Here's a pro tip: Don’t just focus on what your competitors do. Pay close attention to what they don’t do. A rival clinic might have a clunky online booking system or a three-week wait for new appointments. Those are your strategic openings.

Spotting Market Gaps and Trends

A solid market analysis goes beyond just your direct competitors. You need to look at broader industry trends and see how they apply to your local area. For example, telehealth isn't going anywhere. Could you attract busy patients with virtual consultations? Is there a growing local interest in niche services like functional medicine or IV therapy that legacy clinics are ignoring?

Take the U.S. primary care market, for instance. It's projected to hit a market size of $370.8 billion in 2026, with around 133,000 practices in operation. You can find more financial insights and market data on ibisworld.com.

That massive growth points to huge demand, but it also signals major pain points like physician burnout and long wait times. Patients are actively looking for better options. Your business plan needs to show exactly how you’ll capitalize on these trends to offer a more personal, efficient, and patient-focused experience that carves out your own profitable slice of the market.

Designing Your Operations and Technology Framework

This is where the rubber meets the road.This is where the rubber meets the road. You've done the market research and defined your vision; now it’s time to build the engine that will run your practice day in and day out. Your operations and technology framework is that engine, and a well-thought-out plan shows investors you've moved beyond the "what" and are deep into the "how."

Think of this section as the blueprint for your clinic's daily life. It needs to map out every single step of the patient journey, from how they first find you online to how they pay their final bill. Getting this right isn’t just about being efficient—it’s about creating a seamless experience that makes patients want to come back and tell their friends.

Mapping Core Clinical and Administrative Workflows

A great practice runs on clear, repeatable processes. You don't need to write a 100-page manual, but you do need to show you understand all the moving parts. Start by outlining the big-picture workflows.

What are the critical touchpoints you need to define?

- Getting Patients in the Door: How does someone go from a stranger to a new patient on your schedule? Is booking an appointment easy and digital, or are they stuck playing phone tag and filling out paper forms?

- The Visit Itself: What happens when the patient walks in? Detail everything from the check-in process and the clinical consultation to how you’ll handle charting and documentation.

- Getting Paid: Map out the entire revenue cycle. This means everything from submitting an insurance claim and fighting denials to processing a simple copay.

- Keeping Patients Engaged: The relationship doesn't end when they leave. How will you manage follow-ups, handle prescription refills, and communicate with them long-term?

This initial analysis, which starts with understanding your patients and what your competitors are doing, is foundational.

As the diagram shows, a deep dive into your market directly informs the operational systems you need to build. It’s all connected.

Building Your Modern Technology Stack

The technology you choose will either become your greatest asset or your biggest headache. The old way of doing things—stitching together 8-12 different software programs for your EHR, billing, and patient portal—is a recipe for disaster. It creates security risks, frustrates your staff, and grinds your practice to a halt.

It’s no surprise that medical groups are pouring money into better IT. In fact, 30% of practice leaders say it's their second-largest new budget item. This trend isn’t about chasing shiny objects; it's a strategic shift away from clunky, fragmented systems toward unified platforms that just work. For anyone writing a business plan today, this means showing you’ve chosen a single, integrated ecosystem that can handle everything from booking to billing. You can see more on this trend in the full MGMA report on medical group spending.

An integrated tech stack isn't a luxury anymore; it's a competitive necessity. When your patient booking system talks directly to your EHR, which then communicates seamlessly with your billing platform, you eliminate hours of manual data entry and dramatically reduce the risk of costly errors. This is the foundation of a scalable practice.

The goal here is a single source of truth for all patient and operational data. It makes your team insanely efficient and provides a clean audit trail, which is non-negotiable for HIPAA compliance. You can learn more about picking the right tools in our guide to healthcare practice management software.

Defining Key Staffing Roles and Responsibilities

Even the best technology is useless without a great team to run it. In this part of your plan, you need to outline the core team you’ll need to get off the ground. You don’t need to have every person hired, but you absolutely need to define the roles and what they’ll be responsible for.

Start with a simple, lean org chart. It should include:

- Clinical Staff: Think physicians, nurse practitioners, and medical assistants. What are their specific duties in patient care and documentation?

- Administrative Staff: This includes your practice manager and front desk coordinators. Detail their responsibilities for scheduling, billing, and keeping patients happy.

- Specialized Roles: Depending on your services, you might need an aesthetician, a dedicated billing specialist, or even a part-time marketing coordinator.

For each role, write a brief job description outlining their key duties and the qualifications you're looking for. This proves you have a solid plan for building a team that can execute your vision and deliver top-notch care from the moment you open your doors.

Building Your Financial Projections and Funding Plan

This is where the rubber meets the road in your business plan for a medical practice. A powerful mission and a brilliant market analysis are fantastic, but without solid, believable numbers to back them up, they're just ideas. Your financial projections prove that your practice isn't just a passion project—it's a viable, profitable business.

Let’s be honest: investors and lenders will spend more time on these spreadsheets than any other part of your plan. They're looking for a realistic financial story that shows you've thought through every dollar, from the cost of exam tables to your revenue forecast in year three. This is your chance to build serious confidence in your venture.

Detailing Your Startup Costs

Before you can dream about future profits, you need an exhaustive, line-by-line list of your initial, one-time startup costs. I've seen too many new practice owners make the mistake of underestimating this number. It’s a critical error that can strain cash flow from day one and put the entire business in jeopardy.

As a rule of thumb, always build a contingency fund of at least 15-20% into your budget. Trust me, unexpected expenses will pop up. Construction delays, extra permit fees, or higher-than-expected equipment quotes are more common than not.

Here are the big-ticket categories you absolutely must detail:

- Real Estate & Build-Out: Think lease deposits, renovation costs to meet clinical standards, and any architectural or design fees.

- Medical & Office Equipment: List everything. I mean everything—from specialized lasers for a medspa to the computers, phones, and chairs in the waiting room.

- Initial Inventory: What clinical supplies, medications, or retail products do you need stocked before you can open your doors to the first patient?

- Licensing & Legal Fees: Factor in business registration, professional licenses, credentialing with insurance panels, and attorney fees for lease reviews and setting up your business entity.

- Technology & Software: This includes your EHR/EMR system, practice management software, patient portal setup, and basic IT infrastructure.

The numbers you present must tell a story of diligence. A lender can spot an unrealistic budget from a mile away. If your equipment estimate is a single, round number, it screams that you haven't actually gotten quotes from vendors. Detail and specificity are your best friends here.

A well-researched financial breakdown is essential. Here’s an illustrative example of what this could look like for a new medspa, helping you think through the specific costs you'll need to account for in your own plan.

Sample Startup Cost Breakdown for a Boutique Medspa

| Expense Category | Estimated Cost Range | Notes & Considerations |

|---|---|---|

| Lease Deposit & Build-Out | $25,000 – $75,000+ | Varies widely based on location and the condition of the space. Includes plumbing, electrical, and room configuration. |

| Medical Equipment (Laser, etc.) | $70,000 – $200,000+ | The largest capital expense. Get multiple quotes. Consider leasing vs. buying for high-cost devices. |

| Furniture & Fixtures | $15,000 – $30,000 | Includes treatment beds, reception desk, waiting room seating, and office furniture. |

| IT & Software (EHR/PM) | $5,000 – $15,000 | Covers initial setup fees for software, computers, printers, and network installation. |

| Initial Inventory & Supplies | $10,000 – $25,000 | Injectables, skincare products, disposables, linens, and clinical supplies. |

| Legal & Licensing Fees | $5,000 – $12,000 | Attorney fees for entity formation/lease review, business licenses, and professional board fees. |

| Marketing & Grand Opening | $10,000 – $20,000 | Website development, branding, initial ad spend, and promotional events to launch your practice. |

| Working Capital (6 months) | $75,000 – $150,000 | Crucial cash reserve to cover payroll, rent, and other operating expenses until you are cash-flow positive. |

| Contingency Fund (15%) | $32,250 – $79,050 | Your safety net for the unexpected costs that will inevitably arise. Don't skip this. |

| TOTAL ESTIMATED STARTUP | $247,250 – $606,050+ | This range demonstrates why specific, vendor-quoted numbers are essential for an accurate and defensible plan. |

This table is just a starting point, but it highlights the level of detail needed to build a credible financial model that instills confidence in potential investors or lenders.

Crafting Realistic Revenue Projections

Once you've nailed down your startup costs, it's time to project your income for the first three years. Optimism is great, but realism is what gets you funded. Your revenue forecast should be built from the ground up, based on conservative assumptions about patient volume and your service pricing.

Start by figuring out your practice's true capacity. How many patients can you realistically see per day? From there, you can model your revenue based on your mix of services and what you expect to collect, whether from insurance reimbursements or your cash-pay price list.

A smart way to present this is with three different financial scenarios:

- Conservative Case: Your baseline, assuming patient growth is slower than you hope. This shows you have a plan to survive if things get off to a slow start.

- Expected Case: This is your most realistic projection, directly tied to your market analysis.

- Best-Case Scenario: An optimistic view if your marketing hits a home run and patient volume exceeds your initial expectations.

Presenting multiple scenarios shows foresight and proves you're a responsible financial planner. For a deeper dive into managing your practice's day-to-day finances, our guide on bookkeeping fundamentals offers some essential tips to get you started on the right foot.

Projecting Your Ongoing Expenses and Profitability

With revenue modeled, you can now build your pro forma profit and loss (P&L) statement. This is the document that subtracts your ongoing monthly expenses from your revenue to show your projected profitability over time.

Be meticulous when listing your expenses:

- Fixed Costs: These are the predictable bills—rent, staff salaries and benefits, malpractice insurance, and software subscriptions.

- Variable Costs: These fluctuate with patient volume—things like medical supplies, marketing spend, credit card processing fees, and utilities.

It's also crucial to show that you understand the broader financial pressures in healthcare. Medical cost trends continue to climb, with some analyses like PwC’s detailed healthcare industry analysis projecting an 8.5% increase for the Group market. While there's some good news for independent practices, the landscape is still tough. A strong business plan must show how you’ll navigate these headwinds, likely through smart, efficient operations.

Justifying Your Funding Request

Finally, it's time to connect all the dots. Your funding request shouldn't feel like a number pulled out of thin air. It should be the direct sum of your total startup costs plus an operating reserve to cover your expenses for the first six months (or until you hit your break-even point).

Clearly spell out exactly how you'll use the money. For example, specify that $150,000 is for specific medical equipment, $50,000 is for leasehold improvements, and $75,000 is for working capital. This level of detail demonstrates that you're a meticulous planner and a responsible steward of capital. It transforms your financial section from a simple list of numbers into a compelling argument for investment.

Common Questions on Medical Practice Business Plans

Even after going through a step-by-step guide, you're bound to have some lingering questions. That's completely normal. Let's tackle some of the most common ones I hear from physicians and practice managers.

Think of this as a final gut-check before you put your plan in front of a lender, investor, or partner.

How Often Should I Update My Plan?

Your business plan isn't a "set it and forget it" document. It's a living roadmap. I always tell my clients to pull it out for a quick review at least once a year. This helps you see if you're hitting the financial and operational goals you laid out.

A full-blown rewrite, however, is probably necessary every 2-3 years. You'll also need to do a major update if something big changes.

Think about triggers like:

- You're going after a new round of funding to expand.

- You're adding a major new service, like aesthetics or a cash-based wellness program.

- It's time to open a second location.

- There's a big shift in healthcare regulations or how insurance pays for your services.

Keeping it current ensures the plan remains your guide for the future, not just a dusty record of the past.

What Is the Biggest Financial Mistake to Avoid?

I see this one all the time: wildly optimistic revenue forecasts paired with dramatically underestimated expenses. Lenders and investors have reviewed hundreds of these plans. They can spot unrealistic numbers from a mile away, and it’s the quickest way to kill your credibility.

To sidestep this trap, you have to root every single number in reality. Base your revenue projections on conservative patient numbers and use real, verifiable reimbursement rates for your specialty in your specific geographic area. When it comes to expenses, be meticulous. List everything—salaries, malpractice insurance, marketing, software subscriptions—and then add a 15-20% contingency fund on top of it for the inevitable surprises.

The real power of your financial projections isn't in big, flashy numbers. It's in their defensibility. When you can point to the research and real-world data backing up every line item, you build incredible trust with anyone reading your plan.

How Much Detail on Technology Is Necessary?

Get specific. Really specific. These days, your technology is the central nervous system of your practice. It controls your efficiency, your patient experience, and your ability to stay compliant. Simply writing "we'll use an EHR system" just doesn't cut it anymore.

Instead, explain the type of system you’ve chosen and, more importantly, why it’s the right fit for how you plan to work. Lay out your strategy for patient communication, online appointment scheduling, and billing. The key is to show how these different pieces will work together. A plan that highlights a unified, integrated platform demonstrates that you have a sophisticated understanding of what it takes to run a modern medical practice.

Does My Business Plan Really Need a Marketing Section?

Yes. Absolutely. It's non-negotiable. Your marketing strategy is what proves you have a concrete plan to actually attract and retain patients. It shows you’ve thought about how you’re going to generate revenue from the moment you open your doors.

You don't need a 100-page marketing manifesto, but you absolutely must cover the essentials:

- Your Target Audience: Who is your ideal patient? Be specific.

- Key Channels: Where will you find them? (Think local SEO, physician referrals, social media, community events).

- Brand Messaging: What makes your practice different, and why should a patient choose you over the competition?

- A Preliminary Budget: How much are you realistically setting aside for marketing in your first year?

Including this shows that you've considered the entire business cycle, not just the clinical side of things.

A solid business plan is the foundation for a thriving practice, and the right technology partner makes executing that plan possible. Ragnar STACK provides a vertically integrated ecosystem that eliminates the complexity of managing multiple vendors, allowing you to focus on patient care. Learn more at https://notes.rstack.io.

Share This Story, Choose Your Platform!

LISTEN NOW

CAPTIVATING READS

Our blog is packed with articles and stories based around lifestyle, business, design and wellbeing. Subscribe now to get all of our updated directly to your inbox every week.